What is double materiality ?

Definition & challenges

Dual materiality represents a paradigm shift in the approach to extra-financial performance. Unlike traditional materiality analysis, which considers only one perspective, it integrates two complementary and inseparable dimensions to assess the strategic relevance of your ESG issues.

If you are new to this subject, we invite you to read our article dedicated to the definition of double materiality: Double materiality: what are we talking about?

Why is dual materiality transforming the ESG strategy ?

Adopting a dual materiality approach is much more than just regulatory compliance. In fact, it is a strategic performance driver at several levels.

First, it allows move from a defensive logic to an opportunity vision. Rather than considering ESG and its challenges as simple risks to be mitigated, the double materiality reveals how sustainability can create value: new markets linked to the ecological transition, loyalty of committed employees, differentiation through positive impact, reduction of operational costs through energy efficiency, etc.

Then she strengthens your credibility with investors and funders. Financial players are increasingly integrating ESG criteria into their capital allocation decisions. A rigorous double materiality analysis demonstrates your ability to identify and manage extra-financial risks that could affect your valuation. It facilitates access to sustainable financing and improves your ESG rating.

Double materiality also contributes to the improvement of your strategic management. By objectively prioritizing your ESG issues according to their real relevance, you focus investments and efforts on the topics that really matter, for you and for your stakeholders. No more “sprinkled” CSR strategies: you are building a targeted, meaningful and impacting roadmap.

At last she Anticipates international regulatory changes. From France to Europe, extra-financial reporting frameworks converge on this dual approach. By adopting double materiality now, you get ahead of your future obligations and avoid costly (and tedious) overhauls of your reporting system.

How to carry out an effective double materiality analysis ?

Conducting a rigorous double materiality analysis requires a methodology structured in five key steps. Each of them determines the quality and relevance of your final results. It is therefore necessary to make every effort to carry it out correctly.

Step 1: identify your key stakeholders

Any analysis of double materiality is based on dialogue with your stakeholders. They determine what is “material” or not, based on their expectations, concerns and their influence on your business.

Start with map your entire ecosystem : employees, customers, suppliers, investors, shareholders, shareholders, shareholders, local communities, local communities, local communities, NGOs, regulators, regulators, business partners (business providers), unions, media, etc. Don't forget the internal stakeholders that are often overlooked, such as employee representative bodies or audit committees.

Afterwards, prioritize these stakeholders according to two criteria:

- Their influences on your organization (ability to affect your decisions, your reputation, your results).

- Their reliance to your organization (degree of impact of your activities on them).

An Influence/Dependency Matrix allows you to segment your stakeholders into 4 categories, such as:

- Stakeholders wrenches (strong influence, strong dependence) that justify thorough consultation,

- Stakeholders strategic (strong influence, low dependence) to be informed regularly,

- Stakeholders impacted (low influence, high dependence) whose concerns must be taken into account,

- Stakeholders peripherals to be monitored without excessive mobilization.

For key and strategic stakeholders, define appropriate consultation methods: individual interviews with managers and investors, working groups with operational teams, digital surveys for employees and customers, sector panels for suppliers, etc. Here, the objective is to gather their vision of priority ESG issues for your sector and your company.

Step 2: data collection (or, the crux of the matter)

The quality of your dual materiality analysis depends directly on the reliability and comprehensiveness of your data. This collection phase is often the most time-consuming, but it is absolutely decisive.

For the impact dimension, you need to gather data on your environmental and social externalities.

- On the environment side: energy consumption, greenhouse gas emissions (scopes 1, 2 and 3), water consumption, waste production, use of critical resources, biodiversity on your sites, etc.

- Social side: headcount and turnover, work accidents, occupational accidents, training provided, pay differences, diversity of management bodies, working conditions in the value chain, fiscal contribution by territory, etc.

For the financial dimension, collect data that allows you to assess how ESG issues affect your business model. This includes: geographic and sectoral exposure to climate risks, dependence on rare or volatile resources, costs related to environmental regulations, investments in R&D for the transition, market shares on sustainable products, risk premiums applied by your insurers and funders, etc.

Les data sources are multiple :

- Interns : management systems (ERP, HRIS), financial reporting, operational data, employee surveys, internal audits

- Sectoral externals : professional benchmarks, sectoral materiality studies published by standardization bodies, analyses of your competitors

- Regulatory and scientific : public databases (Ademe, IEA, IPCC), academic studies, climate risk assessments

Common mistakes to avoid : do not define the scope of collection (which legal entities? what activities?) , neglecting scope 3 of carbon emissions (often 80% of the total footprint), limiting yourself to easily accessible data while ignoring material but undocumented issues, confusing quantity and quality (10 reliable indicators are better than 50 approximate ones), and not involving operational teams who hold field information.

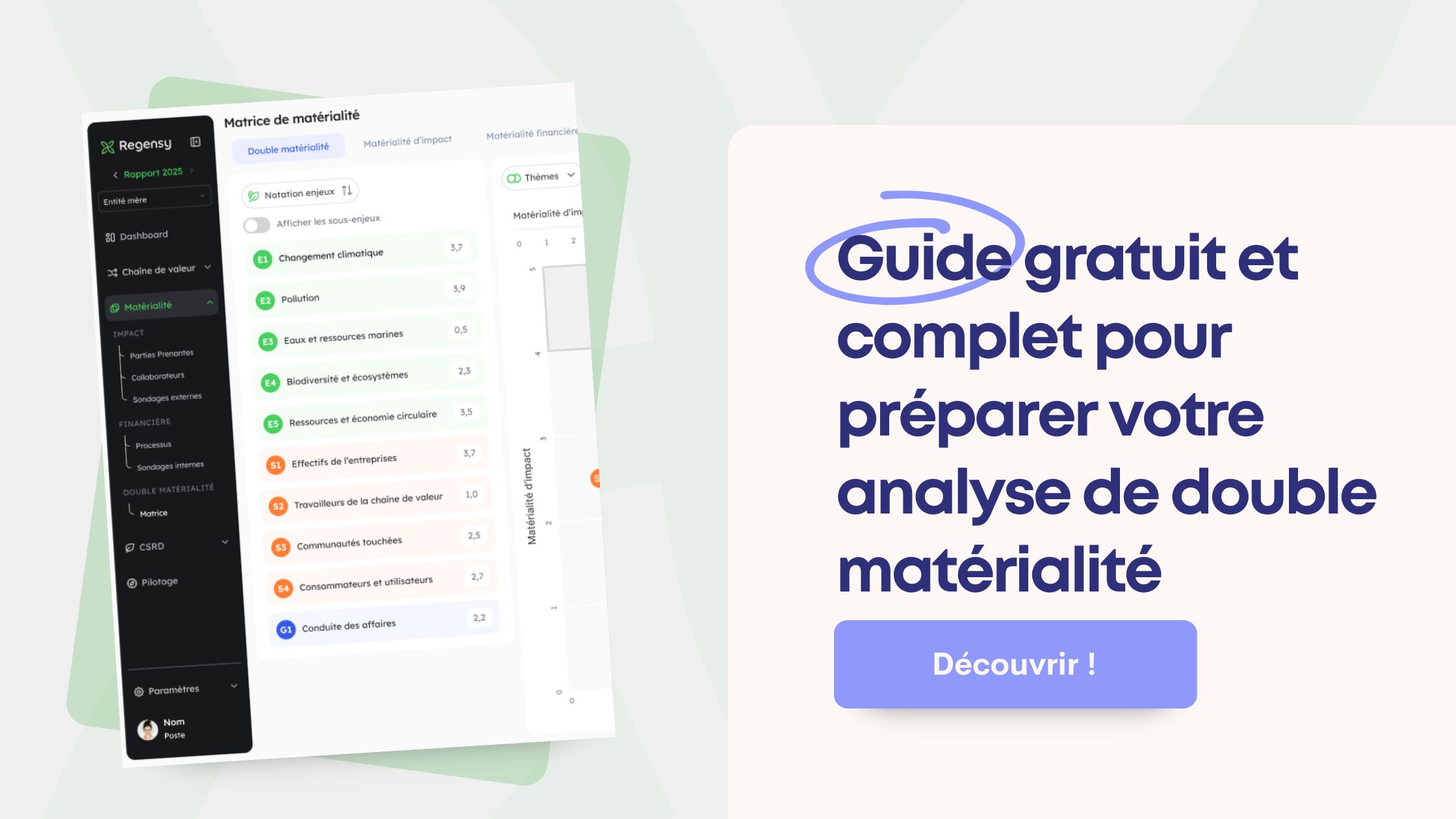

Automate your data collection with Regensy - 30-day free trial →

Step 3: assess impacts and risks

Once your data has been collected and your stakeholders consulted, you must score each ESG issue according to the two dimensions of materiality. This assessment combines a quantitative approach (based on data) and a qualitative approach (based on surveys and consultations).

For impact materiality, assess each issue according to:

- THEscale of the impact: how many people, ecosystems or territories are concerned?

- THEextent : what is the intensity of this impact? Is it negligible, significant, or major?

- The character irremediable : can the impact be reversible or is it permanent?

- La probability Occurrence if the impact is potential

For example, the scope 3 emissions of a transport company have a broad scale (global atmosphere), a significant extent (contribution to global warming), a partially irremediable nature (persistence of CO2) and a certain probability (daily activity).

For financial materiality, evaluate according to :

- La magnitude financial: what amount of turnover, margin or assets is concerned?

- La probability Occurrence of risk or opportunity

- THETime horizon : short term (5 <3 ans), moyen terme (3-5 ans) ou long terme (> years)

Use a standardized scoring grid, for example from 1 to 5, for each criterion. The final grade can be a grade point average or a multiplicative combination depending on your methodology. The main thing is to be consistent and transparent about the calculation rules.

Here are some concrete sectoral examples :

Banking and insurance sector : the risk of climate transition obtains a moderate impact score (the bank does not issue much directly) but a very high financial materiality (massive exposure via credit portfolios to carbon sectors, risk of asset devaluation, regulatory changes on capital requirements).

Textile sector : working conditions in the supply chain obtain a high impact score (millions of workers concerned, risks of human rights violations) and medium to high financial materiality (reputation risks, customer boycotts, legislative tightening such as due diligence).

Technology sector : the energy consumption of data centers obtains a significant impact score (substantial carbon footprint) and increasing financial materiality (energy costs, decarbonization obligations, expectations of corporate customers on the footprint of their cloud services).

Step 4: Building your double materiality matrix

The double materiality matrix is the synthetic visualization of your analysis. It positions each of your ESG challenges on two axes: impact materiality (vertical axis) and financial materiality (horizontal axis). If you want a specific reminder of what this is about, we invite you to read our dedicated article: Double materiality: what are we talking about?

Matrix structure : draw two perpendicular axes, generally graded from 1 to 5 or from low to high. Each ESG issue is represented by a dot or a bubble whose size may reflect a third criterion (for example the urgency of action). Use color coding to distinguish between E, S, and G dimensions.

Strategic areas :

- Upper right quadrant (strong double materiality): challenges that are simultaneously impacting and financially material. These are your absolute strategic priorities that justify significant resources and management at the executive level.

- Upper left quadrant (high impact materiality only): issues with a high external impact but a low direct financial consequence. They are part of your social responsibility and can become financially material in the long term.

- Lower right quadrant (strong financial material only): business risks or opportunities without major external impact. Example: cybersecurity, diversity on the board of directors.

- Lower left quadrant : issues of lower priority to be monitored but not justifying major investments.

Example of an annotated matrix for an agri-food company:

Strong double materiality (upper right quadrant):

- Scope 3 GHG emissions (agriculture)

- Sustainable water management in areas of water stress

- Nutritional quality and health of products

- Traceability and food safety

High impact materiality (upper left quadrant):

- Working conditions for agricultural producers

- Animal welfare in the supply chain

- Imported deforestation (palm oil, soybeans)

Strong financial materiality (lower right quadrant):

- Commodity price volatility

- Compliance with new labelling regulations

- Attracting and retaining talent in a tight market

Add annotations directly on the matrix to explain certain counterintuitive positions or to specify the perimeters. This visualization becomes your strategic communication tool with the board of directors, investors, and operational teams.

Step 5: validate and communicate the results

Your analysis is only valuable if it is validated by the right authorities and appropriate by the teams that will have to implement it.

Internal validation process :

- Technical validation : have your scoring methodologies and calculations reviewed by your CSR, finance and risk teams to ensure the accuracy of the scope, analyze and lock in the robustness of the insights

- Business validation : present the results to the operational departments concerned to verify that the issues identified correspond to the realities on the ground

- Strategic validation : submit the final matrix to the executive committee and then to the board of directors for alignment and commitment

- External validation : in some sectors, a review by an independent third party (auditor, consulting firm) reinforces credibility

Restitution formats according to audiences :

- For the board of directors : one-page executive summary + visual matrix + top 5 priority issues with strategic and financial implications

- For investors : structured document detailing methodology, results, action plans and monitoring indicators

- For employees : educational infographic explaining the material challenges and the expected contribution of each

- For external stakeholders : publication in the annual report or the universal registration document, with transparency on methodological limits

Integration into the global strategy :

The analysis of double materiality should not remain a theoretical exercise. It should inform your decision-making processes:

- Definition of ESG objectives and management KPIs

- Prioritization of CSR investments and sustainable innovation

- Construction of strategic planning scenarios

- Risk assessment through internal audit and risk management

- Criteria for evaluating suppliers and partners

- Financial and extra-financial communication

Plan to update your analysis now: material challenges evolve with your strategy, your sectoral context and societal expectations. An annual or biannual update is generally recommended.

Start your free and non-binding analysis for days 30 days with Regensy ➜

Dual materiality matrix: interpretation and strategic use

Building your matrix is just the beginning. Knowing how to interpret it and transform it into concrete actions differentiates organizations that make double materiality an exercise in compliance from those that use it as a performance driver.

Understanding the four quadrants of your matrix

High priority zone: strong double materiality (upper right quadrant)

The challenges positioned in this quadrant combine significant impact on the environment or society AND material financial consequences for your business. These are your priority strategic issues which should be included in your executive management roadmap, subject to quantified objectives, dedicated budgets and regular reporting to the board of directors.

Actions to be taken:

- Define ambitious and measurable goals with specific deadlines

- Appoint an executive sponsor (member of COMEX) for each major challenge

- Allocate significant human and financial resources

- Integrate key managers and managers into the variable remuneration

- Communicate actively internally and externally about your commitments and progress

- Develop strategic partnerships to accelerate solutions

Typical examples: decarbonization of the value chain, circular economy, water management in areas of water stress, product safety, ethics and diversity of governance.

Impact materiality zone only (upper left quadrant)

These challenges generate significant environmental or social impacts but do not yet (or not significantly) translate into direct financial risks or opportunities. They fall under your social responsibility and your positive contribution beyond the immediate economic interest.

However, be careful: these challenges may migrate towards strong double materiality under the effect of regulatory changes, NGO campaigns, social movements or new customer expectations. A proactive approach avoids crises and positions your business favorably before competitors.

Actions to be taken:

- Set goals for progress even without immediate financial pressure

- Implement monitoring systems to anticipate changes in financial materiality

- Investing in innovation and experimenting with solutions

- Strengthen transparency and dialogue with relevant stakeholders

- Documenting your efforts to build your reputational capital

Typical examples: animal welfare (depending on sectors), human rights in the supply chain (as long as no reputational crisis has existed), contribution to local development, biodiversity on certain sites.

Financial materiality zone only (lower right quadrant)

These challenges present business risks or opportunities without generating major external impacts. They fall under the risk management And of theoperational efficiency, but do not constitute ESG issues in the traditional sense.

Actions to be taken:

- Integrate into your traditional risk management processes

- Define mitigation plans or strategies for seizing opportunities

- Follow up using the usual financial and operational management tools

- Communicate primarily with investors and financial analysts

Typical examples: cybersecurity, technological innovation, attraction of rare talent, diversity of advice (depending on context), general regulatory compliance.

Low materiality zone (lower left quadrant)

These challenges are neither strongly impacting nor financially material in your specific context. This does not mean that they are uninteresting, but they do not justify priority investments or dedicated strategic management.

Actions to be taken:

- Maintain a watch to detect changes in materiality

- Apply best practices and minimum regulations

- Documenting for extra-financial reporting but without a dedicated program

- Reallocate resources to material challenges

Attention to subjectivity: an issue may be of low materiality overall but critical on a site, a subsidiary or a specific business segment. Adapt your approach according to local contexts.

From matrix to action: examples of practical cases

Case 1: manufacturing industrial group (15,000 employees)

Their analysis of double materiality has positioned decarbonization as a strong double materiality: a strong contribution to emissions (significant scope 1 + 2, major scope 3 via suppliers) AND high financial materiality (increasing carbon tax, expectations of contracting customers, access to conditional green financing).

Actions deployed :

- Objective of reducing scope 1+2 emissions by 50% by 2030 (vs 2020) included in the strategic plan

- Creation of a position of Carbon Transition Director reporting to the General Manager

- Annual budget allocated for energy efficiency, renewable energies and process electrification

- Supplier program with carbon scoring integrated into 100% of tenders

- 15% of the variable remuneration of 200 key managers indexed to the achievement of carbon objectives

- Quarterly reporting to the board on progress and bottlenecks

Results that can be measured after 2 years : -22% in scope 1+2 emissions, 3 major customers signed thanks to the low-carbon offer, access to a €200M green credit line with a 0.3% subsidized rate, ESG ranking improved from B to A-.

Case 2: service and consulting company (3,000 employees)

Their analysis identified talent attraction and retention as materially financial (high turnover, difficulty recruiting, training costs) but with moderate social impact (generally good working conditions, low-risk sector).

Actions deployed :

- Flexible remote work program and a 4.5-day week with no pay reduction

- Investment in training courses and internal mobility

- Transparency on pay differentials and reduction plan

- Strengthening social dialogue and quarterly well-being surveys

- Management positions open primarily to internal promotions

Results that can be measured after 18 months : turnover reduced from 23% to 15%, employee satisfaction score increased from 3.4/5 to 4.1/5, 30% reduction in recruitment costs, productivity maintained despite the reduction in working hours.

Case 3: distribution group (45,000 employees, 850 stores)

The analysis positioned the circular economy (repairability, reuse, recycling) as a strong double materiality: direct environmental impact (waste, resources) AND financial materiality (new customer expectations, savings, new potential revenues).

Actions deployed :

- Launch of an in-store repair offer for 15 product categories

- Reconditioned product corners in 100% of stores

- Partnership with social and solidarity economy actors for collection and repackaging

- Elimination of non-recyclable plastic packaging on 100% of private label products

- Mobile application allowing customers to resell their used products for a voucher

Results that can be measured after 3 years : 35,000 repairs carried out avoiding 850 tons of waste, refurbished offer generating 45M€ in additional turnover, customer satisfaction on environmental commitment +18 points, reinforced brand image among 18-35 year olds.

ESG double materiality: how to integrate it into your strategy ?

Dual materiality analysis reveals your priority challenges, but it is its integration into your management processes that really creates value. The dual materiality of ESG then becomes the basis of your sustainability strategy.

Aligning dual materiality and ESG goals

Once your material challenges have been identified, translate them into SMART strategic objectives (Specific, Measurable, Achievable, Realistic, Time-defined). This transformation of the matrix into an operational roadmap is decisive.

Define relevant KPIs for each material issue:

- KPIs should measure both your performance (impact reductions, improvements) and your exposure to risk or financial opportunity

- Choose indicators that are already used in your sector to facilitate benchmarking

- Combine absolute indicators (tons of CO2, m³ of water, number of accidents) and relative indicators (carbon intensity per unit produced, frequency rate, diversity ratio)

- Distinguish between internal management KPIs (monitored monthly) and external communication KPIs (reported annually)

Examples of translation issues → goals → KPI :

Hardware issue : decarbonization of the value chain

Strategic objective : reduce scope 1+2 emissions by 55% and scope 3 emissions by 30% by 2030 vs 2020

Management KPI : absolute emissions and carbon intensity/M€ CA, share of renewable energies, number of suppliers committed to SBTi

Related financial KPI : energy savings achieved, cost per ton of CO2 avoided, interest rate premium obtained on green financing

Hardware issue : working conditions and health and safety

Strategic objective : zero serious accidents by 2027, maintaining the frequency rate under 5

Management KPI : frequency/severity rate of accidents, number of days lost, rate of participation in safety training, site audit results

Related financial KPI : direct/indirect costs of accidents, insurance premiums, absenteeism rates

Prioritize action plans based on 4 criteria:

- The level of materiality (double strong > simple > weak)

- The benefit/cost ratio (quick wins vs. heavy long-term investments)

- Interdependencies (certain actions create co-benefits on several issues)

- The emergency (regulatory deadlines, stakeholder tensions)

Build a multi-year roadmap with clear milestones: what should we have achieved in 1 year, 3 years, 5 years? Who is responsible for each construction site? What resources are needed? This planning turns your dual materiality analysis into a real actionable ESG strategy.

Measuring progress over time requires discipline and rigor:

- Establish a regular review schedule: quarterly for operational management, annual for strategic assessment

- Document progress but also the bottlenecks and adjustments needed

- Consistently compare yourself to initial goals and to the sector benchmark

- Celebrate successes to keep teams engaged

- Update your matrix at least every 2 years to incorporate changes in context

Involve teams in the process

The success of your ESG dual materiality strategy depends on the commitment of the entire organization. Without collective ownership, even the most rigorous analyses remain a dead letter.

Role of senior management : executive support is critical. The CEO and the COMEX must publicly promote the approach, integrate it into strategic communications, allocate the necessary resources and make difficult decisions when short-term and long-term trade-offs occur. The appointment of a Chief Sustainability Officer (CSO) reporting directly to the CEO sends a strong signal on the strategic importance given to material challenges.

Commitment of operational staff : the field teams have the concrete levers for action. Divide strategic objectives into operational targets by department, site or business unit. Integrate ESG KPIs into individual and collective objectives, with significant weight (10 to 20% minimum). Organize workshops to co-construct action plans: employees are more accepting of the changes they have helped to define.

Create working groups or networks of “ESG referents” in each entity to increase expertise, facilitate the sharing of best practices and maintain momentum. These ambassadors are the link between corporate strategy and local realities.

Training and awareness-raising : not everyone has the same level of maturity when it comes to ESG issues. Deploy adapted training courses:

- Basic modules for all employees (why the double materiality, what are the challenges for our company, how each contributes)

- In-depth training for managers and strategic support functions (finance, purchasing, sales, HR)

- Advanced expertise for dedicated teams (life cycle analysis, carbon footprint, extra-financial reporting)

Vary the formats: e-learning for mass distribution, face-to-face workshops for in-depth exchanges, serious games for fun appropriation, feedback to anchor in concrete situations. The objective is to develop a true culture of double materiality where everyone understands the links between their daily actions, the impact of the company and its overall performance.

Avoid the classic pitfalls of double materiality analysis

Even with good intentions, some recurring mistakes weaken the quality and credibility of your analysis. Here are the main pitfalls to avoid:

- Confusing comprehensiveness and relevance : wanting to identify 50 material issues dilutes your focus. An effective matrix generally has 10 to 20 significant challenges. Beyond that, you are dispersing your resources and losing strategic readability.

- Let availability bias dominate : issues for which you easily have data tend to be overvalued, while those that are less documented are minimized. Fight against this trend by investing in data collection on emerging or complex topics (scope 3, biodiversity, human rights in the supply chain).

- Underestimating the consultation of external stakeholders : an analysis built only internally reflects your own perceptions, not necessarily those of your stakeholders. External consultations often reveal blind spots and allow you to challenge your hypotheses.

- Ignoring emerging issues : limiting yourself to the challenges that are already mature in your sector makes you miss out on subjects that will become material tomorrow. Integrate a prospective dimension: what challenges currently low materiality could change under the effect of regulatory, technological or societal changes?

- Do not document the methodology : without transparency on your methodological choices (scope, scoring criteria, weightings), your analysis lacks credibility and cannot be reproduced for future updates. Document each step and justify your decisions.

- Forget the financial dimension : many companies are well versed in impact assessment (simple traditional materiality) but struggle to quantify the financial implications. Work closely with your finance and risk management teams to reinforce this dimension.

- Producing a static matrix : your double materiality analysis must live and evolve. Plan from the start the update cycles, the methods of integrating new data, the triggers that would justify an early revision (acquisition, change of scope, major new regulations).

Regulatory vigilance points : reporting frameworks are multiplying and evolving rapidly. Ensure that your methodology remains compatible with the standards applicable to your organization: GRI (Global Reporting Initiative), ESRS (European Sustainability Reporting Standards), IFRS S1/S2, TCFD, etc. Anticipate the external insurance requirements that are becoming widespread on material extra-financial information.

What tools can you use to simplify your double materiality analysis?

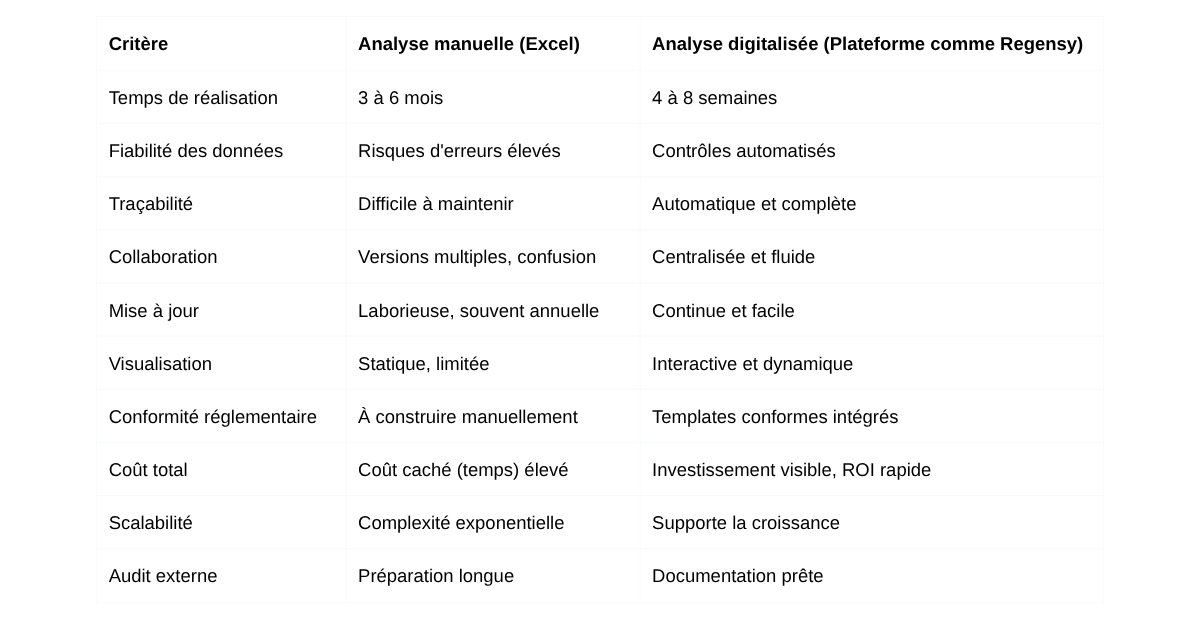

Faced with the methodological complexity and the extent of data collection, equipping yourself with a dedicated digital solution is quickly becoming essential. Excel spreadsheets quickly reach their limits in terms of traceability, collaboration and reliability.

Why digitize your analysis process?

- Time savings and data reliability : a dedicated platform structures your data collection according to standardized frameworks, considerably reduces manual re-entries and the risk of error. What took 3 to 6 months in manual mode can be done in 4 to 8 weeks with the right tools. Teams spend less time compiling data and more time analyzing data and defining action plans.

Automated calculations (carbon emissions, water consumption, social indicators) eliminate formula errors and guarantee methodological homogeneity between the various entities. Built-in consistency checks detect anomalies and inconsistencies before they affect your results.

- Traceability and continuous updating : each data entered is time stamped, sourced and versioned. You know who entered what, when, and on what basis. This traceability is essential for external audit and to justify your declarations to regulators and investors.

Digitalization also allows for continuous updating rather than an annual “photo”. You manage your material challenges in real time, quickly identify drifts and adjust your strategy with agility. Your dual materiality matrix becomes a dynamic management tool, not a simple reporting document.

- Easier collaboration between teams : an analysis of double materiality mobilizes multiple contributors: CSR, finance, operations, purchasing, HR, legal, communication. A collaborative platform centralizes exchanges, assigns tasks, monitors progress and avoids multiple versions of files circulating by email.

Configurable workflows automate validation circuits: a contributor enters → his manager validates → the CSR team consolidates → the management approves. Everyone only accesses the data and functionalities relevant to their role, guaranteeing confidentiality and relevance.

The essential functionalities of a high-performance solution

- Automated data collection : the platform must allow import from your source systems (ERP, HRIS, energy management systems) via API or standardized files. It should also offer guided entry forms for data that cannot be automated, with built-in consistency checks.

The connectors to the reference databases (Ademe emission factors, energy conversion grids, sectoral ratios) automatically enrich your data and ensure methodological alignment with international standards. - Real-time matrix modeling : the solution must automatically calculate the materiality scores according to your methodology (which you must be able to configure), position the issues on the matrix and allow simulations: what happens if I change the weight of this criterion? What if this risk materializes? This ability to script is valuable for testing the robustness of your analysis.

The visualization must be interactive: filters by E/S/G dimension, by entity, by time horizon, zoom on certain issues, history of positioning changes. You must be able to instantly generate different views according to your audience (board of directors, investors, operational teams). - Reporting and export : the platform automatically generates the necessary reports and dashboards: executive summary, sustainability report, regulatory declarations, investor communications. The templates must be customizable according to your graphic charter and your specific needs.

Exports to Excel, PowerPoint or PDF facilitate sharing with external stakeholders who do not have access to the platform. Exporting raw data also allows for additional analyses in your own business intelligence tools. - Collaborative management : notification system to alert contributors of the tasks assigned to them, comments and annotations to facilitate contextual exchanges, history of changes to understand data evolution, granular rights management to secure access to sensitive information.

The solution must also integrate project management functionalities: stage planning, progress monitoring, identification of bottlenecks, project risk management. Double materiality analysis is a business project that requires rigorous management.

Manual analysis vs. digital analysis

Try Regensy free for 30 days - No commitment, no credit card →

FAQ: your questions about double materiality

How long does a double materiality analysis take?

The duration varies according to the size of your organization, your ESG maturity and the tools used. For a first complete analysis, count:

- With manual approach : 3 to 6 months for an SME (< 500 people), 6 to 12 months for a multi-site group

- With digital platform : 4 to 8 weeks for an SME, 2 to 4 months for a complex group

The data collection phase generally represents 40 to 50% of the total time. Equipping a dedicated solution considerably accelerates this aspect. Update analyses are then much faster: 2 to 4 weeks with the right tools and processes in place.

Who should be involved in the analysis ?

An effective double materiality analysis requires a multidisciplinary project team:

- Executive sponsor : member of COMEX to lead the process and arbitrate

- Project manager : generally the CSR/Sustainable Development Director

- Core team : representatives of key functions (finance, risks, operations, legal, HR)

- Business contributors : experts on each ESG issue identified

- External stakeholders : representative panel for consultations

Also plan for a steering committee meeting monthly to validate the guidelines and unlock possible obstacles. The early involvement of the board of directors (or the ad hoc committee: audit, CSR) facilitates final validation.

What is the difference between simple materiality and double materiality ?

Simple materiality (or pure financial materiality) takes a unique perspective: how do ESG issues affect a company's financial performance? This is the approach traditionally preferred by investors and accounting standards (such as IFRS S1/S2 standards).

Double materiality adds a second perspective: how does the company impact the environment and society? It recognizes that businesses have a responsibility beyond simply creating value for their shareholders. An issue can be material in one or both dimensions.

Concrete example: a bank that finances fossil projects generates significant climate impacts (impact materiality) AND is exposed to risks of asset devaluation and loss of customers (financial materiality). It is an issue with a strong double materiality. Conversely, diversity on the board of directors can be financially material (better governance, innovation) without major external impact: simple financial materiality.

How often should you update your analysis ?

Full update : every 2 to 3 years in a stable context, every 1 to 2 years in a context of rapid change (sector in transformation, strong growth, major new regulations). This comprehensive update revisits all potential issues, consults stakeholders again, and revises the methodology as required.

Light refresh : annually to refresh the materiality scores for the issues already identified, integrate new performance data and adjust the positioning at the margin. This update does not call into question the overall structure but maintains the relevance of the matrix.

Extraordinary review : in the event of a major event that substantially changes your context (significant acquisition or sale, major ESG incident, disruptive regulatory change, sudden change in stakeholder expectations). Don't get stuck on outdated analysis.

With a digital platform, these updates are much less cumbersome since the data is collected continuously and the calculation methodologies are already set up. This is a strong argument in favor of digitalization.

How to prioritize the issues identified ?

Three levels of prioritization are superimposed:

Level 1 - According to materiality : The challenges of strong double materiality are priority by nature. They justify most of your resources and attention. The challenges in terms of simple materiality (impact or financial) come next. Low materiality issues are monitored but without dedicated programs.

Level 2 - Depending on the emergency : With equal materiality, prioritize short-term issues (< 3 years) over long-term ones, issues under imminent regulatory pressure, and those subject to strong tensions with key stakeholders.

Level 3 - Based on the cost/benefit ratio : Identify “quick wins” (high impact, low investment, quick results) to generate momentum and visible successes. Balance with longer-term structuring projects that permanently transform your model.

Use an effort/impact matrix to visualize these trade-offs: vertical axis = materiality and expected benefits, horizontal axis = complexity and required resources. Build a balanced portfolio of projects rather than focusing all of your resources on a single issue.

Turn Your Dual Materiality Analysis Into Competitive Advantage

Dual materiality is no longer an option but a must for any organization concerned about its sustainability. Far from being a theoretical compliance exercise, it is a great strategic lever: clarification of your ESG priorities, alignment of your teams, strengthened credibility with your stakeholders, and informed management of your sustainable transformation.

Businesses that master their dual materiality analysis get ahead of their competitors. They anticipate risks, capture opportunities, attract talent and capital, and build long-term resilience in a rapidly changing world.

Methodological and operational complexity should not hold you back. With the right methodology, the right tools and appropriate support, you can carry out a robust and actionable analysis in a few weeks, then integrate it sustainably into your strategic management.

Regensy was designed precisely to simplify and accelerate your dual materiality approach. Our platform guides your team step by step, automates data collection, generates your matrix in real time, and facilitates collaboration between all your stakeholders. Hundreds of companies trust us to structure their ESG strategy and gain impact.

Start your double materiality analysis in 48 hours with Regensy

Free 30-day trial - No commitment - No credit card